The Only Road That Doesn't Go Through a Toll Booth

What if the real move isn't choosing the right side of the system — but stepping off the disk entirely? A framework for sovereign trade in an age of permissioned money.

Consider a pencil.

Not as metaphor — as supply chain. The graphite in its core may come from Sri Lanka or China. The cedar casing from the forests of the American Northwest. The metal ferrule from a zinc-copper alloy produced somewhere in an industrial corridor you will never visit. The rubber eraser from a plantation in Malaysia. The paint — that cheerful yellow — from a pigment compound assembled across multiple sourcing agreements you couldn't trace if you tried.

The pencil costs less than a dollar. And yet it is, as Leonard E. Read observed in his celebrated 1958 essay I, Pencil, the product of a global coordination so vast and so spontaneous that no single human mind planned it, no government directed it, and no central authority approved it. It happened because millions of people — none of them trying to make a pencil — made choices that, in aggregate, produced one.

Now ask a different question: what happens to that pencil when every transaction in its chain passes through a toll booth?

What happens when each link in that chain requires a bank account, a government-issued identity number, a KYC compliance check, a monitored wire transfer, and a fee extracted by an intermediary who produced none of the pencil's materials and performed none of its labor?

The pencil still gets made. But someone, at every step, takes a percentage. And that percentage compounds. And the debt that funds the currency those percentages are denominated in compounds further. And the interest on that debt — the usury at the root of the entire system — demands that the system grow continuously just to service its own existence.

The pencil is still made. But its maker is permanently behind — not because they failed, but because the road they were forced to use has a toll at every mile.

This essay is an attempt to name the alternative road. Not a political alternative — not a different party, a reformed central bank, or a more enlightened regulatory framework. A geometric alternative: a road that does not pass through the center of the system at all, because it runs along the outside of it.

That road has a name. It is the agora.

I. The Inversion of Authority

Most people in the United States have inherited an inverted model of authority. In the common imagination, power flows downward: from federal government to state, then county, then city, and somewhere at the bottom of that stack — the individual. This inversion is not a minor error in civic education. It is a category error that changes everything downstream.

The original compact was structured the other way around. At its foundation sits what the founders variously called natural law, self-evident truth, or the endowment of the Creator — a source of rights that precedes and supersedes any political arrangement. From that foundation flow the people, who are not subjects of the compact but its beneficiaries. And from the people flows a delegated, limited authority — the government — which exists entirely to serve the compact's beneficiaries, not to own them.

The correct order is:

Natural Law / God — Source of inherent rights. Not delegated, not negotiated. Prior to any compact.

The People — Beneficiaries of the compact. Not subjects. The principal authority from which government derives its mandate.

The State (all levels) — Trustee. Holds only delegated authority. Manages on behalf of the principals.

The legal language for this relationship is trustee and beneficiary. A trustee holds authority over assets not for their own benefit but for those of the people they serve. They possess no inherent power. They manage. The moment a trustee begins behaving as an owner — demanding permission, controlling access, surveilling conduct, extracting rents — they have violated the foundational terms of the arrangement.

Applied to commerce, this distinction has a sharp edge. When the state requires a citizen to present a government-issued identity number to open a bank account, to send money across a border, to participate in trade — it is not functioning as a trustee. It is functioning as a gatekeeper. And a gatekeeper extracts a toll.

Think of it this way: you hired a property manager to look after your house while you travel. Reasonable enough. But imagine you come home one day and the property manager demands to see your ID before letting you in. That is not property management. That is occupation.

That is what KYC — Know Your Customer requirements — does to trade. It takes a trustee relationship and inverts it. Suddenly you need permission from your own employee to conduct your own business.

The United States already acknowledged one domain where the state's reach ends: religion. The separation of church and state is not merely a legal technicality. It is a structural recognition that some spheres of human life are categorically beyond the state's jurisdiction. The logic of that recognition applies equally to trade. If the people are the beneficiaries — not the subjects — of the governmental compact, then the tools they use to exchange value with one another belong in the same protected zone as the tools they use to seek meaning.

This is not a radical proposal. It is the logical extension of a constitutional framework that already exists.

We call it the separation of business and state.

II. The Geometry of the Trap

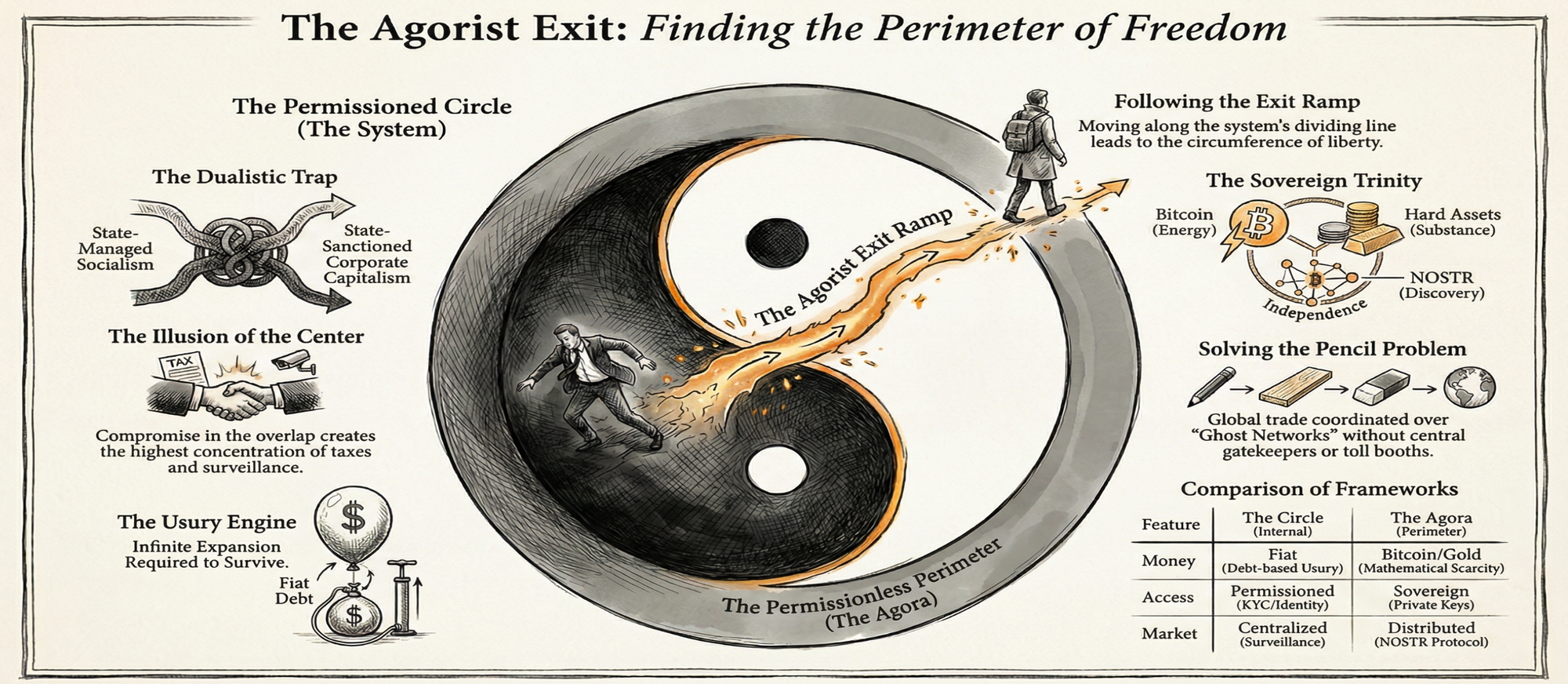

To explain why most attempts to escape the debt-based system fail, it helps to think geometrically.

Most political and economic arguments present themselves as a choice between two options. Left or right. Capitalism or socialism. Hard money or fiat. The sophisticated position, we are told, is to find the sensible middle — the overlap, the synthesis, the both-sides-have-a-point zone.

Picture a Venn diagram: two circles overlapping. The left circle is state-controlled money. The right circle is market-controlled money. The overlap — the purple zone — is where most reform proposals live: managed currencies, gold standards with central bank oversight, regulated stablecoins, social democracy. People argue fiercely about how large the overlap should be and which direction it should lean.

But here is what the Venn diagram obscures: the overlap is still inside both circles. You have not left the system. You have found a comfortable position within it.

Now replace the Venn diagram with the yin-yang. This is a richer model, because it captures what the Venn diagram misses: the two forces are not separate. They interpenetrate. Each side carries the seed of its opposite. The line between them is not a wall but a dynamic interface — that flowing S-curve at the center.

Most people, confronted with the yin-yang, believe the correct position is on that center line. Balance. Integration. The golden mean. And at first glance, the geometry seems to support this.

But follow the center line further. Don't stop at the middle.

The S-curve of delineation does not terminate at the center of the circle. It continues. It flows outward in two directions, curving as it goes, until it reaches the outer edge of the symbol — the circumference that contains both yin and yang.

A person who follows that line all the way out is not straddling the two forces. They are standing on the boundary of the system that produced those two forces. And beyond that boundary is something the system does not own.

Open space. The agora.

This is the geometric shift at the heart of sovereign agorism. Not a third way — a third way is still inside the circle. An outside way. The agorist does not choose between the two permitted options. They exit the system of choices entirely.

Why the Color Matters

In agorist theory, this space is often called the gray market. That word choice is precise. If the outside is drawn as pure white space, it accidentally aligns with the white half of the yin-yang — one of the very two forces we are trying to exit. Gray is neutral. And there is a quiet irony in it: mix black and white and you get gray.

The exit is not a new side. It is what happens when you refuse the forced choice entirely.

III. The Money Trilemma

Every monetary system is attempting to solve three problems at once. Almost none solve all three simultaneously — not because the engineering is poor, but because solving the third problem tends to threaten the interests of those who profit from the first two.

The three problems are value (does this money represent something real, or is it a promise that can be broken?), velocity (can this money move quickly across distances and borders?), and sovereignty (can a person use this money without permission, surveillance, or the threat of confiscation?).

Fiat currency moves fast and is universally accepted — but its value is a political promise, not a physical fact, and its use is monitored, gatekept, and freezeable. Two out of three.

Gold and silver hold real value across centuries — but they are heavy, slow to move, and hard to divide cleanly at global scale. One out of three.

Bitcoin moves fast and requires no permission — but it has no physical anchor. Its scarcity is mathematical, not geological. Two out of three — a different two than fiat.

Kinesis (gold-backed crypto) gets value and velocity — but requires government-issued ID at the gate. Two out of three again. Same two as fiat, different packaging.

Notice what gets sacrificed first in every case: sovereignty. Fiat sacrifices it structurally — the surveillance and KYC apparatus is built in. Gold sacrifices it practically — you cannot send a bar of metal to a graphite miner in Sri Lanka without involving a company, a customs agent, and a bank. Kinesis sacrifices it deliberately — it chose corporate compliance over permissionless access. Bitcoin gets closest, but without a physical anchor, it remains vulnerable to the accusation that it is simply a more elegant form of fiat: valuable because people agree it is, not because the Earth's crust produced it at great cost.

This is not a reason for despair. It is a map. Each failure points precisely at what the next iteration needs to preserve.

IV. The Sovereign Trinity

The framework that emerges from mapping those failures is not a single tool. It is a three-layer architecture — each layer solving for what the others cannot accomplish alone.

₿ Bitcoin — The Engine

Value moves instantly, anywhere, without a bank, a banker's approval, or an identity check. Fixed supply. Mathematically finite: 21 million coins, each divisible into 100 million satoshis. The engine does not expand. It deepens. Faith in math — not in men.

⚖ Hard Assets — The Anchor

Gold, silver, land, commodities — things the Earth produced at genuine cost that cannot be printed, inflated, or promised into existence. The physical anchor that gives the digital layer a tether to reality no central bank can cut.

⬡ NOSTR — The Agora

A protocol — not a platform — for permissionless communication and discovery. The lead miner and the woodcutter find each other here, without an intermediary who can delete, freeze, or identity-check the conversation. No central server. No account approval. Just keys and relays.

Together, these three layers form a closed loop outside the yin-yang of the permissioned system.

Bitcoin without NOSTR is an engine with no roads — you have the capacity to move value but still need a centralized marketplace to find who you're moving it to. NOSTR without Bitcoin is a conversation with no currency — people can find each other permissionlessly but still have to pay through a toll booth. Hard assets without digital rails are gold bars at the wrong address — real value stranded by the friction of physical distance.

The trinity is not three separate tools. It is one circuit.

Money alone isn't enough. A marketplace alone isn't enough. You need the full loop — the circuit that closes entirely outside the permissioned system.

A note on NOSTR specifically, because it is the least understood of the three. The instinct people bring to NOSTR is to compare it to a messaging app or a social platform with different politics. But NOSTR is not a platform. It is a protocol. The difference is structural. A platform is owned — it has a server that can be seized, a company that can be pressured, a terms-of-service that can be changed. A protocol is mathematics. It exists as long as two people agree to speak its language. You cannot seize it. You cannot KYC it. You can only use it — or not.

V. Why Bitcoin Is Not Fiat — And Why It Matters

A reasonable objection to Bitcoin as the engine of a sovereign economy is that it seems to share fiat's essential problem: its value is derived from collective agreement rather than physical substance. You cannot hold a satoshi. It does not corrode, conduct electricity, or sit in a vault. In what sense is "faith in math" meaningfully different from "faith in government"?

The answer lies in the mechanism — specifically, in the direction of growth.

Fiat currency is a system of infinite expansion. Because it is created as debt — banks lend money into existence, and interest is owed on the amount created — there must always be more money tomorrow than there is today, just to pay the interest from yesterday. The supply must expand continuously. An expanding supply means a diluting unit of value. Every hour you worked for a dollar last year is worth fractionally less this year. The treadmill is not an accident. It is the arithmetic.

Bitcoin is a system of infinite inversion. Its total supply is fixed — 21 million coins, a hard ceiling written into the protocol's mathematics. But each coin is divisible into 100 million satoshis, and those satoshis can be divided further as needed. The system does not grow outward by adding more units. It grows inward through divisibility.

A growing economy does not require more money. It requires the existing money to become more valuable per unit as the goods and services it represents multiply.

Think of it this way:

Fiat is a ruler made of elastic. Every time the government adds debt, the inch gets shorter. You can measure things with it — but your measurements of wealth drift constantly downward even when you do everything right.

Bitcoin is a ruler made of steel, marked in 100 million increments. You can cut it into smaller and smaller pieces, but the total length of the steel never changes. The inch stays an inch.

This is not a philosophical preference. It is a structural difference in how value is stored across time.

A currency that must expand to function is a currency that must, by design, transfer wealth from those who hold it to those who issue it. Every round of inflation is a tax on savings. Every new unit issued dilutes every existing unit. The expansion benefits those closest to the point of issuance — banks, governments, large borrowers — at the expense of those furthest from it: workers, savers, small businesses. This is not a conspiracy. It is arithmetic.

VI. The Moral Architecture of Usury

The condemnation of usury is one of the most persistent threads in the history of moral philosophy, crossing traditions that agree on almost nothing else.

Aristotle argued that money is sterile — it is a medium of exchange and nothing more — and that making it breed by charging interest on loans violates its nature. The Quran prohibits riba — the taking of interest — in terms that frame it not as impractical but as unjust, a taking from the poor to give to those who already have. Premodern Christian canon law, drawing on both Aristotle and scripture, forbade usury on similar grounds. Even secular philosophical traditions, through thinkers as varied as Proudhon and Gesell, have identified compound interest as a structural mechanism of exploitation.

The persistence of this condemnation across unrelated traditions suggests it is responding to something real — something in the phenomenology of debt-based money that ordinary people feel even when they cannot articulate it technically. That feeling has a name: the sense that no matter how hard you work, you are always behind. That the system requires you to run faster each year just to stay in place. That your savings are slowly stolen from you while you sleep, not through crime but through the ordinary functioning of the financial system.

Trade on the agora's perimeter — in Bitcoin, in hard assets, through NOSTR — is structurally incapable of this dynamic. If you exchange a gold-backed token for a cedar plank, no interest accrues. No debt clock runs. The transaction is complete. One thing of value changed hands for another thing of value. The mathematics of the exchange are closed at the moment of exchange.

This is why the gray market of the agora, which can sound furtive or illicit to ears trained on conventional associations, is in a precise moral sense the cleaner marketplace — not the shadier one. The transaction at the center of the yin-yang, conducted in fiat currency through a surveilled banking system with interest accruing at every node, carries the moral weight of usury. The transaction on the perimeter — peer to peer, value for value, key for key — carries none of it.

The agora is not the black market. It is not the gray market in the sense of legal ambiguity. It is the original market — the ancient Greek agora, which was simply the open space where free people met to exchange things they had made. The state has managed to make that ancient and ordinary act seem radical. That itself tells you something.

VII. On Straddling — A Note on LANA and the Bicycle Problem

Any honest accounting of the current landscape has to grapple with projects that are genuinely trying to move toward the perimeter but remain anchored, however subtly, to the system they are trying to leave.

LANA — the community marketplace concept pursued by projects like LanaLovesExeter — represents something genuinely important: the instinct that trade should be human-scale, trust-based, and rooted in real communities of real people. That instinct belongs on the perimeter. It is correct.

But in its current form, LANA operates like a bicycle with one pedal bolted to the bank's floor. It works with fiat. It tolerates usury as a bridge mechanism. It uses conventional financial rails as an on-ramp, on the theory that you have to meet people where they are before you can take them somewhere new.

There is a philosophical generosity in that theory. There is also a structural problem with it.

The fiat handshake is not neutral. Every transaction that touches the permissioned system creates a data point, a taxable event, a traceable link back to the center of the yin-yang. You cannot be simultaneously sovereign and symbiotic with a system that denies sovereignty. Straddling the line of delineation is not a transitional position. It is a permanent one — because the gravity of the center is continuous, and the moment you extend a hand back toward it, you are being pulled.

| LANA (Current) | LANA Evolved — The Ideal | |

|---|---|---|

| Fiat | Symbiotic — used as bridge | None — fully excised |

| Usury | Tolerates interest rails | Structurally impossible |

| KYC | Partial — some gates | None — private key only |

| Position | Delineation line (S-curve) | Perimeter (the ring) |

| Community instinct | ✓ Correct — preserve this | ✓ Routed through NOSTR |

The DNA of LANA that belongs on the perimeter is the community instinct: find your neighbors, trade what you have for what you need, build trust through repeated exchange, make the agora local before making it global. That instinct, routed through NOSTR for discovery and settled in Bitcoin or hard assets without a corporate intermediary, is exactly the kind of human-scale node the perimeter needs.

The form it takes to get there has to let go of the fiat bridge entirely.

No KYC. No usury. No fiat. These are not three separate requirements. They are three formulations of the same requirement: the hand reaching back toward the center must be released.

VIII. The Pencil, Completed

Return to the pencil. Imagine it assembled now not through the conventional supply chain — bank wires, KYC checks, currency conversions, monitored transfers — but through the sovereign trinity.

The graphite miner posts on a NOSTR relay: "High-grade graphite, available for export, accepting Bitcoin." The message goes out across the relay network — no central server, no account approval, no identity check, just a cryptographic key and a message. The cedar mill sees it. The rubber planter sees it. The pencil maker, wherever she lives, sees all three.

Payments flow in Bitcoin. The values are anchored, if the parties choose, against gold — a commodity settlement layer that gives the satoshi a physical tether the parties trust. No bank clears the transaction. No compliance officer reviews it. No government freezes it because the graphite miner is in a jurisdiction the bank finds inconvenient this year.

The pencil is made. It cost what it costs — the labor, the materials, the coordination — and nothing else. No interest is accruing on the currency used to buy the cedar. No inflation is quietly eroding the savings the miner set aside for next season's equipment. No KYC data is sitting in a database waiting to be breached, sold, or subpoenaed.

This is not a utopia. The pencil maker still faces every ordinary challenge of running a business: finding customers, managing quality, building reputation, navigating the friction of physical logistics. The agora does not eliminate difficulty. It eliminates the toll.

The toll, compounded across a lifetime of transactions, is the difference between building wealth and running in place. It is the difference between a business that grows because its product is good and a business that stagnates because its currency is diluted faster than its margins can expand.

The pencil completed on the agora's perimeter is the same pencil. It was made from the same cedar and the same graphite. But it was made by free people, transacting freely, without asking the system's permission — and without paying the system's toll.

Conclusion: The Perimeter Is Not the Fringe

There is a rhetorical reflex, when any of these ideas are raised, to treat them as fringe — as the province of ideologues or people who distrust institutions for irrational reasons. That reflex deserves examination.

The claim that trade should be voluntary is not fringe. It is the premise of every functioning market economy in history. The claim that money should represent something real is not fringe. It was the global consensus for most of recorded history and was abandoned in 1971 as an administrative convenience. The claim that usury is a moral problem is not fringe. It is among the most widely held ethical intuitions across human cultures, expressed in traditions that share almost nothing else.

What is fringe — what is genuinely radical — is the current arrangement: a global monetary system built on debt issued into existence by private banks, denominated in currencies that governments can devalue at will, tracked and gatekept by a surveillance architecture that treats every transaction as a potential crime until proven otherwise.

The perimeter is not the fringe. The perimeter is where trade used to happen before the toll booths were installed. The agora is old. The surveillance apparatus is new.

What sovereign agorism proposes is not a revolution. It is a return — conducted through modern tools, expressed in modern protocols, denominated in mathematically scarce units rather than political promises.

Bitcoin for the energy. Hard assets for the anchor. NOSTR for the marketplace.

No KYC. No usury. No fiat.

The dividing line between any two permitted choices is not a place to stand. Follow it outward. At the edge, it becomes the circumference. Step onto it, face outward, and you are no longer choosing between the two options the system offers. You are standing on the only road that doesn't go through a toll booth.

The pencil is waiting to be made.

The Three Non-Negotiables

These are not three separate requirements. They are three ways of saying the same thing: that the hand reaching back toward the center of the system must be released.

✗ No KYC — Identity verification for basic trade is the trustee acting as owner. Access to voluntary exchange is a right derived from natural law, not a permission granted by the state. Any tool that demands a government-issued ID at the gate has failed the sovereignty test before it starts.

✗ No Usury — Money that breeds money through interest is structurally exploitative. It requires the system to grow continuously at the expense of those furthest from the point of issuance. Trade on the perimeter is one-for-one: value for value, closed at the moment of exchange, with no debt clock running in the background.

✗ No Fiat — Debt-based currency with an expandable supply transfers wealth silently from those who save to those who issue. Mathematical scarcity — whether geological in gold or protocol-enforced in Bitcoin — is the structural alternative. The inch must stay an inch.

This is a working framework — experimental, in development, and open to revision. It is not financial advice, legal counsel, or a completed system. It is a compass heading: the direction of travel for those who find the toll booths intolerable and the perimeter worth building.

Further Reading

- Leonard E. Read — I, Pencil (1958), Foundation for Economic Education

- Samuel Edward Konkin III — New Libertarian Manifesto (1980)

- Satoshi Nakamoto — Bitcoin: A Peer-to-Peer Electronic Cash System (2008)

- Aristotle — Politics, Book I, Ch. 10 — on the unnaturalness of money breeding money

- Albert O. Hirschman — Exit, Voice, and Loyalty (1970), Harvard University Press

- NOSTR Protocol — nostr.com

- Kinesis Money — kinesis.money/gold

- LanaLovesExeter — lanalovesexeter.co.uk